Taps Coogan – January 27th, 2022

Enjoy The Sounding Line? Click here to subscribe for free.

Enjoy The Sounding Line? Click here to subscribe for free.

Remember, if you will, the Fed’s December 19th, 2018 FOMC meeting when Jerome Powell infamously described the balance sheet runoff as being on “automatic pilot.” That comment, which came as the S&P 500 was already down about 13% from its October highs, sent markets plunging further with the S&P 500 bottoming out on December 26th – 20% down.

Here is Jerome Powell’s famous ‘autopilot’ comment from December 19th, 2018:

“If you go back some years…, people who were working at the Fed in 2013 and 2014 took away the lesson that the markets could be very sensitive to the news about the size of the balance, the pace of asset purchases, the pace of runoff… so we thought carefully about this, how to normalize policy, and came to the view that we would effectively have balance sheet runoff on automatic pilot and use… rate policy to adjust to incoming data and I think that has been a good decision… and I don’t see us changing that and I do think that we will continue to use… rate policy as the active tool of monetary policy.”

The market only bottomed after Fed officials started walking back that line in the following days. Powell famously ‘pivoted’ on January 4th, 2019, suspending further rate hikes and eventually flipping from QT to fresh QE and rate cuts later in 2019. That policy pivot came despite the strongest labor market in a generation and PCE inflation near 2%.

Here is what Jerome Powell had to say Wednesday about the Fed’s soon to be third attempt at reducing its balance sheet in 2022:

“We think of the balance sheet as moving in a predictable manner, sort of in the background, and that the active tool meeting to meeting is not both of them but the Federal Funds rate… I think the pattern we’ll follow is to arrive at a timing and a pace and composition and all those things, and then announce that with advanced notice and it will start in the background and we’ll look to have that running in the background and have the interest rates be the active tool of monetary policy.”

All that’s missing are the words “automatic pilot.”

Tightening didn’t ‘work’ in 2013. It just brought on QE3, the biggest QE program up to that point. Tightening didn’t ‘work’ in 2018 either and brought us Not-QE1 in 2019 followed by Covid and QE-Infinity. Tightening in the exact same way as 2018, but faster, won’t ‘work’ in 2022.

From the beginning of the above quote above to the end of his press conference about 40 minutes later, the S&P 500 dropped 2.6%. It’s off again today.

This stuff isn’t rocket science. When the Fed prints money and buys financial assets, financial asset valuation multiples tend to go up. For the fleeting moments when they do the opposite, valuation multiples have tended to go down.

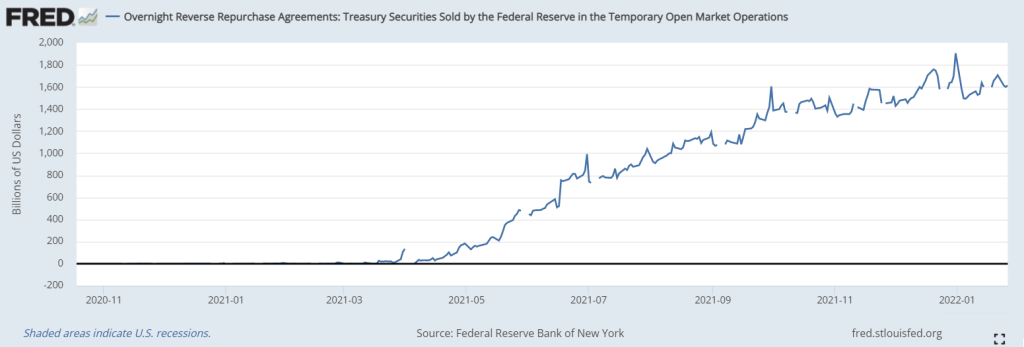

In the excess reserve regime that we have been in since the Global Financial Crisis, the Fed’s balance sheet is monetary policy. The Fed Funds rate is a sideshow. What’s the point of an overnight interbank lending rate for reserves (the Fed Funds rate) when the banks have trillions of dollars of excess reserves? There isn’t one and that’s why the Fed has to do over $1.6 trillion dollars of reverse-repos every day to keep the Fed Funds above zero.

Last time we played this game, the S&P 500 had to drop nearly 20% before the Fed started to seriously backtrack. With CPI inflation at 7%, it’s going to be harder for the Fed to pivot to fresh QE. So far we’ve dropped about 10%. That’s not enough.

Would you like to be notified when we publish a new article on The Sounding Line? Click here to subscribe for free.

Would you like to be notified when we publish a new article on The Sounding Line? Click here to subscribe for free.

So the FED is the stock market and the real economy be damned.

So then based on the economy and the fundamentals what is the “TRUE VALUE” of the stock market?